Back in December 2016 when I started this blog, I wanted to document my journey to Financial Independence. Sure, lifehacks, articles on happiness, investing and side hustles are also important to me. But the core focus of this blog has always been to reach the point where work is optional.

The point where I no longer need to set an alarm in the morning. No longer need to worry about being late or having enough to pay the mortgage, college tuition and holiday getaways. It’s not that I’m sick of the 9-5. I actually like my job which is funny because it seems I’m desperately trying to escape it.

I’m not trying to escape my job. I’m trying to escape the need to depend on my job. That’s entirely different.

So our way of living and working here in London has always reflected that. I’m quite lucky that my partner agreed to shape our life towards this goal. Otherwise, life would’ve been a struggle for sure. But enough of my why of FI. Where do we stand today, September 2019?

We have crossed the halfway point and we’re about 60% there! The green line is staring at me as a lighthouse stares at a ship that’s been travelling for years. Is FI getting real……. for real? :)

Will we defeat the “This will never work” friends comments? Or is the green line a moving target? Will the definition of enough change over time? The good thing about the Work Optional threshold is that it’s set by us. We choose where to set it and how much margin of error to throw into the equation.

I’m starting to believe that reaching financial independence is not just a dream. It’s freakin possible if you put the effort in. It also requires some discipline. I’m also happy that trying to reach for FI has not made our lives miserable.

During this time, we bought (and furnished) a new flat, enjoyed some exotic holidays in the Maldives and Mauritius, went on an amazing US roadtrip while keeping a balanced life when in the UK. Obviously, having a high household income is key to FIREing early. Not spending the majority of your income helps too.

In fact, I believe saving is equally important to having a high income. When you learn how to manage your finances better and run your household like a business, you hone a different skill on the way. I consider the art of frugality to be a very useful one.

The stock market can take your wealth away but not your skills. Therefore being flexible with your spending can be very useful when needed the most in tough times. After all, living paycheck to paycheck leaves zero margin for error really. Get laid off when the boiler breaks down and you’re in trouble.

Managing a growing net worth is a challenge. Being closer to FI than ever, though, brings different questions to mind. Such as, how much can I withdraw from my portfolio every year to never run out of money? I have to rely on protecting my portfolio more than ever. So how do I invest to do that? What if there is no salary to top it up if its value goes down? What is the best asset allocation for my strategy?

Should we purchase private health insurance if we geo-arbitrage our way out of expensive London? What about taxes if I’m no longer a UK resident?

All this matter. But admittedly, they’re good problems to have! :)

How we got there

It would be great to tell you that in 5 years we followed a secret investing strategy that you should follow too. One that can double your money every 3 years and that makes your bank account flex like ‘The Rock’.

But unfortunately, there is no silver bullet. The process we followed to accumulate a good chunk of money in a short amount of time is exactly this:

- Earn a high income

- Spend less than you earn

- Invest the surplus

I wasn’t lucky enough to participate in the UK property boom of the past 20 years. My investment returns were not amazing either given most of our wealth started building up from 2015 onwards. That’s missing half the bull market. But I was lucky enough to invest in bitcoin quickly grow my IT skills and have discipline.

It’s not because we invested in a bull market that brought us closer to FI. It’s because we earned a lot of money and kept most of it.

People will usually focus on how I invest. But high earnings and high savings matter more than investing. If I had to choose between being a good investor vs a good saver I’d always vote for the latter.

Anyway, when you earn 100k a year you’re privileged. But if you earn less than that this doesn’t mean that FI is not possible. It means that it will just take longer. To bring it closer you need to up your skills, ask for a raise or just work more. It’s just math and numbers don’t lie.

That’s it. No silver bullets. Earning a lot of money won’t help though if you spend it on Louis Vuitton and Aston Martins. In fact, depreciating assets will only make things worse as the habit of consumerism kicks in. Focusing on happiness, buying experiences and choosing to DIY instead of outsourcing everything certainly adds up.

I know people on decent salaries that save only 10% because… aren’t you supposed to save 10%? That’s about average. Maybe saving is easier for me thanks to my frugal nature. I don’t subscribe to the cultural norms so it’s kind of intuitive to avoid spending £250 on a Mont Blanc wallet.

No need to show off really, probably because I keep an inner scorecard. Unfortunately, most people like to keep an outer one and that’s an expensive hobby.

So we don’t keep a budget and don’t believe in the latte factor. But we know we can have anything but not everything, and live our lives by this rule. Buying freedom before buying other stuff puts things in perspective. We’re also not afraid of investing regularly, and tapping into the profits of the world’s best businesses as well as property buy-to-lets.

Investing Strategy

I cannot stress enough how important saving is. I always prioritise saving to investing when people ask me for advice. However, there’s only so much you can save plus saving is boring which is why I usually talk about investing. Eventually though, investing is what makes financial freedom possible. Besides, investing is my passion too. So how do I invest?

As the portfolio grows in value, my fear of managing grows with it. I mean… I’m more relaxed about the stock market swings than most people are. I also treated the -20% drop of 2018 as an opportunity to buy shares at a discount. But as the portfolio value increases, the absolute amount of money that can be lost (in £ not % terms) is quite scary!

Plus I did not live the 2009 crash which was probably the worst crash after 1929 in financial history. I am not confident I will stay calm despite the hundreds of articles/books/podcasts I have read on how it feels. Unless you experience it, you cannot know. The answer?

Now that we’ve entered the final 5-year FI window I’m trying to protect our portfolio from the sequence of returns risk. I would definitely want to avoid a scenario where the stock market crashes 6 months after we’ve pulled the trigger and cut our wealth in half! Panic may creep in.

Although there is still a lot more room for the portfolio to grow, I consider protecting what we’ve earned more important than maximizing our return. That said, here’s how our portfolio looks like today:

What’s right for me may not be right for you though. So always consider how risky you want to play it, not just how to earn the most money!

Securities (~60%) is where I invest most of our wealth. That’s a mix of global equities (50%) and bonds(10%). I use a mix of different funds mainly because of early mistakes in picking the simplest one. If I had to start all over again, there would be only 2 funds. One for equities, one for bonds:

I’ve added a few tilts to capture more of the emerging market’s as well as small-cap companies but these are just the icing on the cake. If you’re interested, iShares EM IMI, KBA China A ETF and Vanguard Global Small-cap are the ones making my portfolio a bit more “exotic”.

My Property Partner investments and my flat’s deposit make up the property equity of my portfolio. Despite the fee changes, I would like to increase my investments there. That’s partly to drop the fee percentage but also to take advantage of the massive discounts going on in the resale market right now.

I believe investors are being very emotional following the recent fee hike as well as Brexit. Does this property look like it deserves a -25% discount because of an annual 1% fee and a drop in rental payments?

Property Partner also helps with tax treatment when investing in property as a limited company. Rent is received in the form of dividends which means I receive rent tax-free. This is how taxes work at Property Partner.

Property aside, I also like to keep some cash on the side. 13% may be too much and I’m probably paying for this ‘safety’.

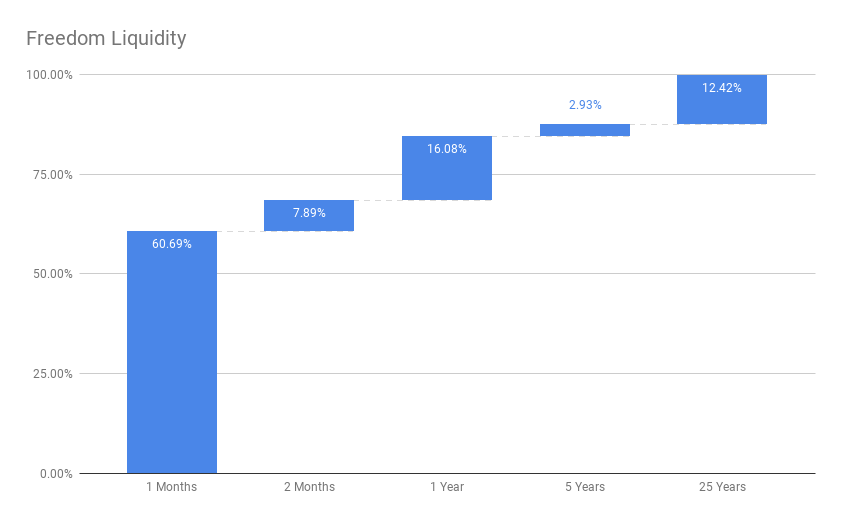

But what I like about our portfolio is that the money is very liquid. Here’s an interesting graph:

{kind=link}

So almost 70% of the portfolio is accessible within 2 months, and 84% within a year.

SIPP is at least 25 years away, and who knows when I will be able to access our pensions given the upward trend! But there are some benefits to having illiquid investments. The main one is that they’re not affecting your behaviour of selling at a loss (or selling at all for that matter)!

How much do I need to retire?

Such a hot question. I plan to answer it in detail as it deserves a post on its own. There are plenty of studies that examine the 100 or so years of stock market history to arrive at one number. The safe withdrawal rate is the maximum amount you can withdraw from your portfolio every year to never run out of money.

For a 30-year or so retirement this is about 4%, although the 4% rule is not very safe. But there are so many variables, such as

- The sequence of market returns (hence the sequence of returns risk)

- Retirement length

- Spending flexibility

- Taxes

Generally speaking, it’s easier to have a variable withdrawal rate that goes up when times are good and down when you need to guard your stock part of the portfolio. Also, contrary to the common belief, the asset allocation should be more conservative when starting retirement and moving to a more aggressive allocation once deeper in retirement.

Anyway, as I said, there’s a post coming on best strategies, withdrawal rates and asset allocation so stay tuned if this boring topic is of interest to you!

So what about us? We’re going to play it risky and depend on a 4% withdrawal rate :O The main idea is that there are always other income avenues such as blogging, matched betting, and perhaps more entrepreneurial hustles down the line that will cover the extra risk.

Knowing myself, why not take advantage of the fact that we will be making a side income as we have always had? We won’t depend on it, but that will act as an extra buffer for splurging or shielding our portfolio even further early on.

I can hear people typing “That’s not retirement Michael!”. Yes, I know it isn’t! I focus more on the FI part of FIRE which gives us options. Certainly, one cannot travel the world for 10 years. Well, not me at least. I want to do stuff, stay creative and help people. Which happens to bring income too.

Plus I don’t plan on stopping the IT work which is both fun and profitable. I just want to have the peace of mind that I don’t have to work if I don’t want to for an undefined period of time.

Being flexible with spending is also key in tough times and I believe we’re comfortable with it.

Share your FI progress in the comments. I’m interested in hearing other people’s opinions.

Foxy Monkey Meetup

I know this is an online blog but there are real people behind all these computers. Which made me think, why not gather everyone at a pub or somewhere and meet each other? This is much better than meeting everyone one-by-one as I’ve done before.

So the first Foxy Monkey meetup is happening, please come along!

Please don’t hesitate! Let’s have a drink, share some helpful tips and have meaningful conversations around personal finance, investing, career, etc.