This is the first post of my Property Partner experiment series. I will be investing £10,000 a year via the Property Partner platform over the next 5 years.

I always wanted to own property as part of my investments. But I was always put off by the hassle that comes with it. Have a high deposit, submit lots of documents to get a mortgage, find tenants, a good estate agency, maintain the property, the high fees and taxes that come with buying/selling… And the list goes on.

Especially now (2018) that London properties have appreciated so much, I think there is little room for growth in the next 5 years ahead.

Areas like Manchester, Liverpool, Birmingham, aka The “Northern powerhouse”, are probably better positioned for capital growth and higher yields. Personally, I have the management problem. How do you remotely manage? And how do you choose a remote tradesperson/estate agent?

To be honest with you, I have not solved that problem but listening to what others say, you have to do the work and build a network of people. Post on property forums that you’re looking for certain skills. Call local agencies, visit occasionally etc. The final reward is there, but it’s a hassle, which is why I have avoided remote property investing so far.

However, I think technology is changing this. I recently started investing via Property Partner by buying a small share in properties there. They do all the work for a 2% fee – sourcing, letting, ongoing management, and you own shares in the property. They pay rent (dividends) monthly and pay the capital growth part as well if investors want to exit.

I find the concept interesting, and although it has many restrictions (you don’t decide how to furnish it, who the tenants are etc) I see lots of advantages too. For example, the option to invest 20% in 5 cities, instead of 1 property in a single city. Liquidity is another – the option to sell your properties anytime in the secondary market to other investors. And obviously avoiding all the buy/sell hassle which is why I didn’t invest in remote property in the first place.

I fully support the modernisation of investments through technology. The world moves on, so the archaic 2-month buy-to-let buying process should evolve too. Airbnb, RateSetter, Uber are just examples of old systems (hospitality, taxi hailing, loan matchmaking) that needed a disruption.

What is Property Partner and why I’m choosing it

In a nutshell, Property Partner is a platform where you can buy and sell shares of properties around the UK. They do the paperwork, find tenants, collect the rent and pay it out to investors. They also welcome investors from abroad.

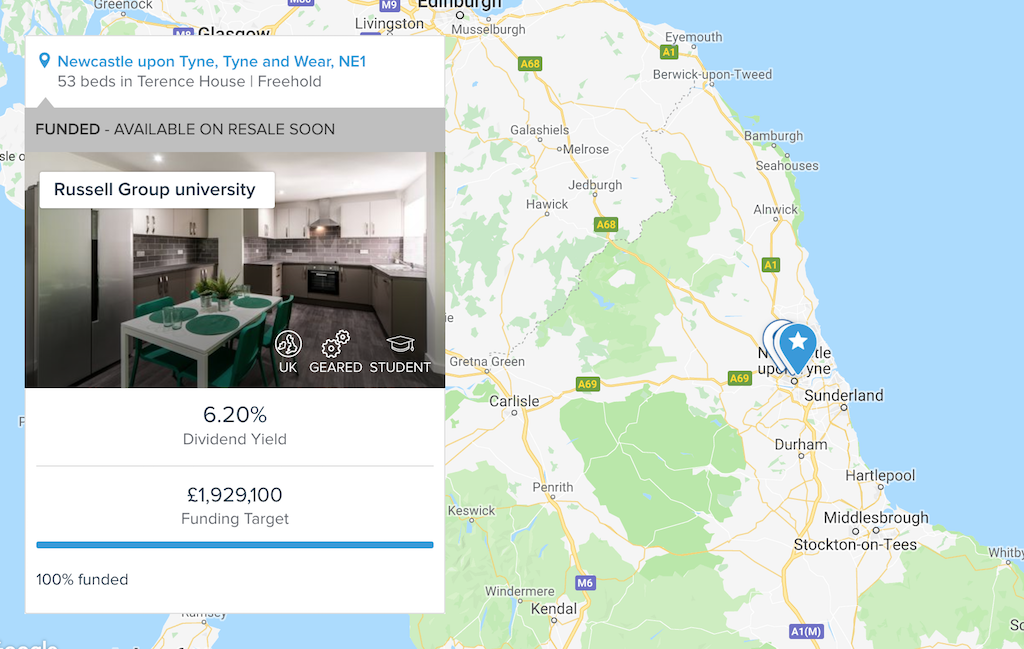

So new deals come up that need funding such as this one:

As you can see this is a student accommodation of 56 units and seeks £1,929,100 in funding (51% LTV). So people can allocate money towards this deal. Once the fund target is met the property is bought.

The 6.2% on the right is the estimated net rent per year. The total return will probably be higher since we haven’t accounted for the (unknown) capital growth from the property appreciation over time. According to PP:

For the 12 months ending Sept 2017, CBRE’s PBSA valuation index showed a total return of 11.9%, outperforming the IPD All Property Index of 9.5% over the same period. It also demonstrated strong rental value growth at 4.1%.

But how do I know the property is worth that much? Turns out independent RICS valuations set the property price and Property Partner try to strike a deal below market value. Since they’re buying in bulk they can negotiate harder.

If you don’t want to DIY you can invest in their managed investment plans. At no extra cost, one can buy a certain characteristics portfolio monitored by PP if you invest a minimum of £5,000. But there is no minimum investment otherwise.

I’ll take up the challenge and try to beat the managed plans by investing solo. I’ll probably lose to the machines… and I won’t blame you if you decide to go for one of those plans. You’ll probably do better.

Do we really own the property?

A new special purpose vehicle (SPV) is formed for every deal that owns the property. According to how much each person invests, they own the equivalent shares in this company.

Therefore, we collectively own the property itself. But that doesn’t mean that we have to collectively make decisions for when to sell (coming up…).

The rent is paid in the form of dividends by the SPV which is why you see “dividend yield” instead of “rent”. If you, like me, are investing via a limited company, dividend payments are music to our ears. They’re tax-free :)

What I love about each deal, is that you can see a clear breakdown of the purchase price, rent, costs (mortgage, sourcing, management) including void periods and taxes. It’s quite transparent.

The first question that comes to mind is this: What if they don’t pay the rent? So I asked this question to the PP guys and here’s the response:

We’re experienced professional landlords, working with carefully chosen third party professional management firms and utilising economies of scale to further improve efficiency. To date we have not underpaid a dividend. If investors ask us for an individual property we can provide an answer as to how many units are let.

Faraj Jabbour, Property Partner

Obviously, you cannot know what will happen in the future but a solid track record is always a good sign.

I confirmed this by looking at the property stats which they openly share in their “Open House” publications. Looking at the one from June 2018, I can download the historic valuation and dividend yield BY PROPERTY!

This is a huge Excel file that for spreadsheet nerds like me is gold. You can plot trends, draw graphs but actually, most of this info can be found in every property online anyway. I highly appreciate the transparency though. If I am to invest serious money here, I’d like to have this sort of detail if need be.

My Property Partner Portfolio

Each person is different. What looks like a bargain to me may look like “bag holding” to someone else.

Before I invested there I asked myself: What do I invest for? High-income? Capital growth or a blend of the two? In such an ultra low interest-rate environment, high yield is amazing. Especially when knowing that Property Partner hasn’t missed out on any rent collection.

But most of the returns in property, historically, come from capital growth. In other words, rent is good, but property appreciation is what makes us the big money. If mortgaged, the gains (or losses!) are boosted.

However, because I chose to invest as a limited company (as opposed to an individual) the rent in the form of dividends is tax-free! Therefore it makes sense for my strategy to lean towards tax-free income while leaving some room for taxable capital growth as well. Let’s cut to the chase.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Whoah! What a Landlord eh? Better not tell the government!!

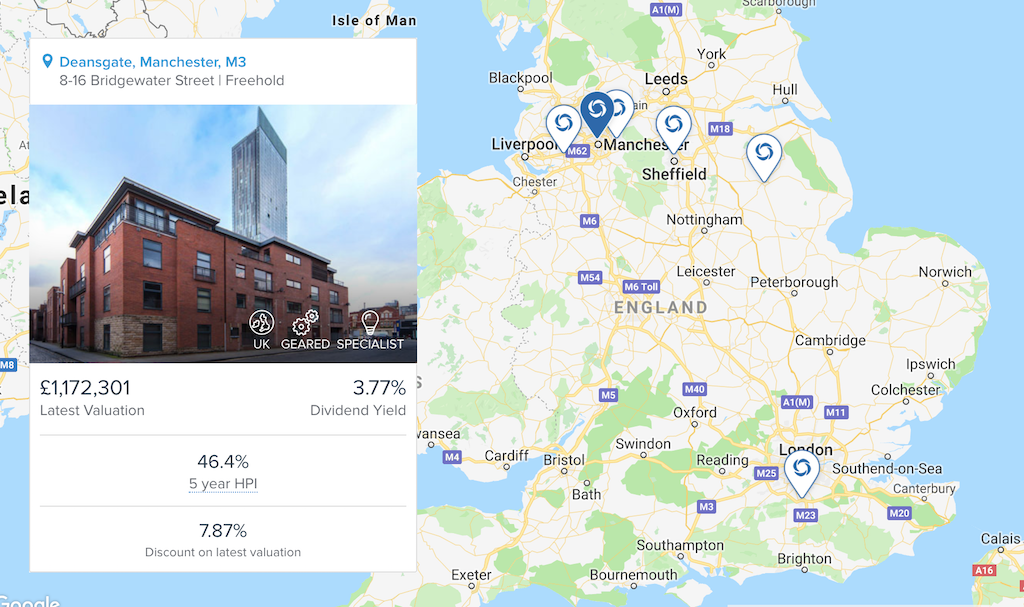

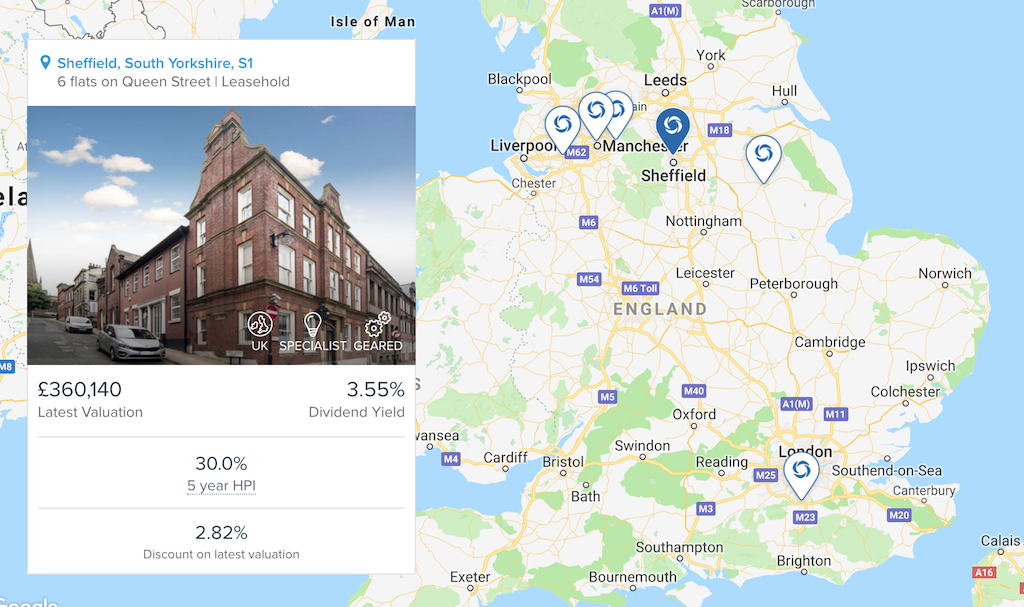

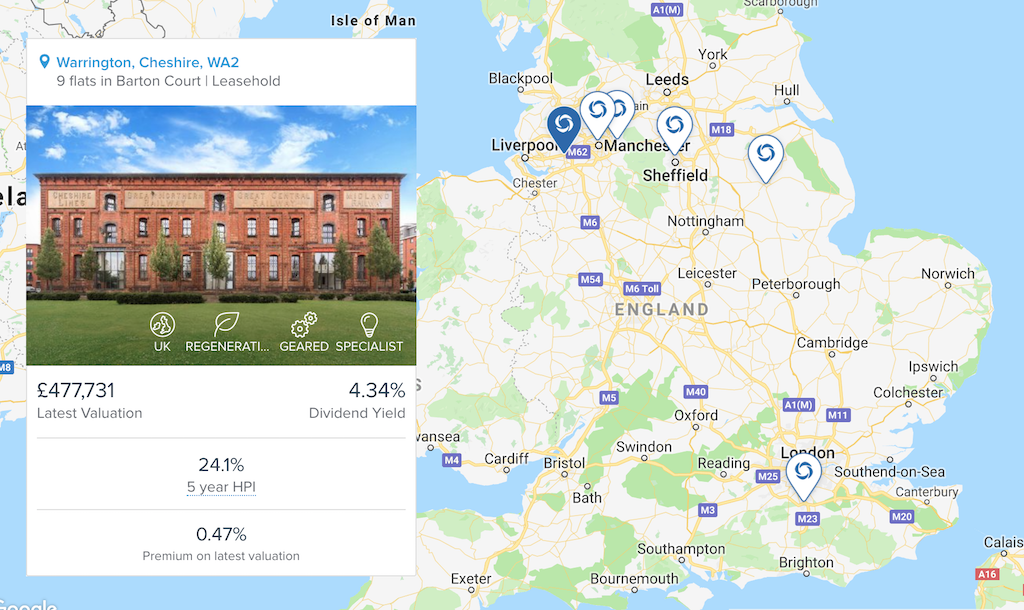

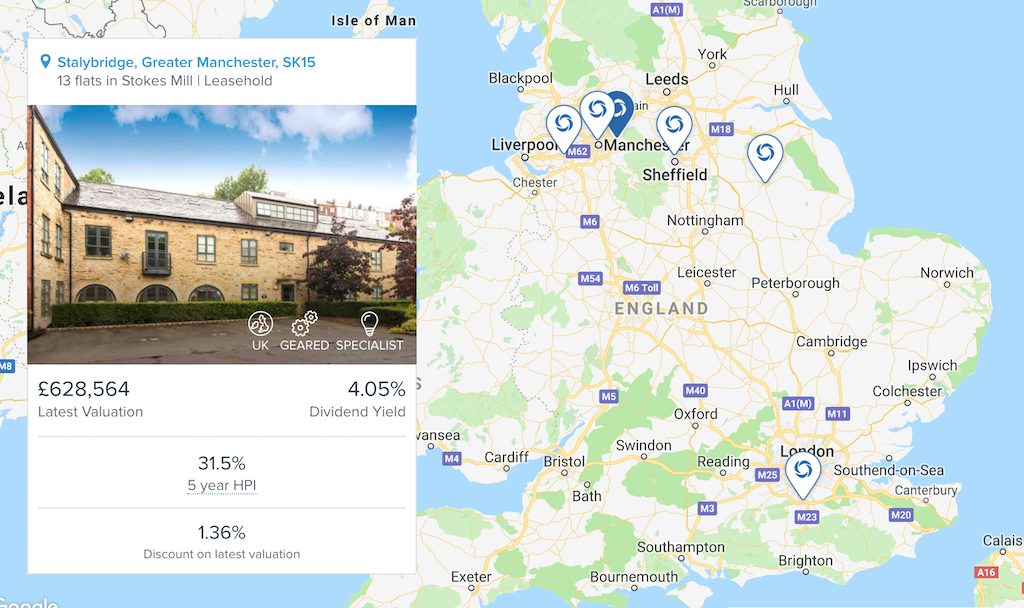

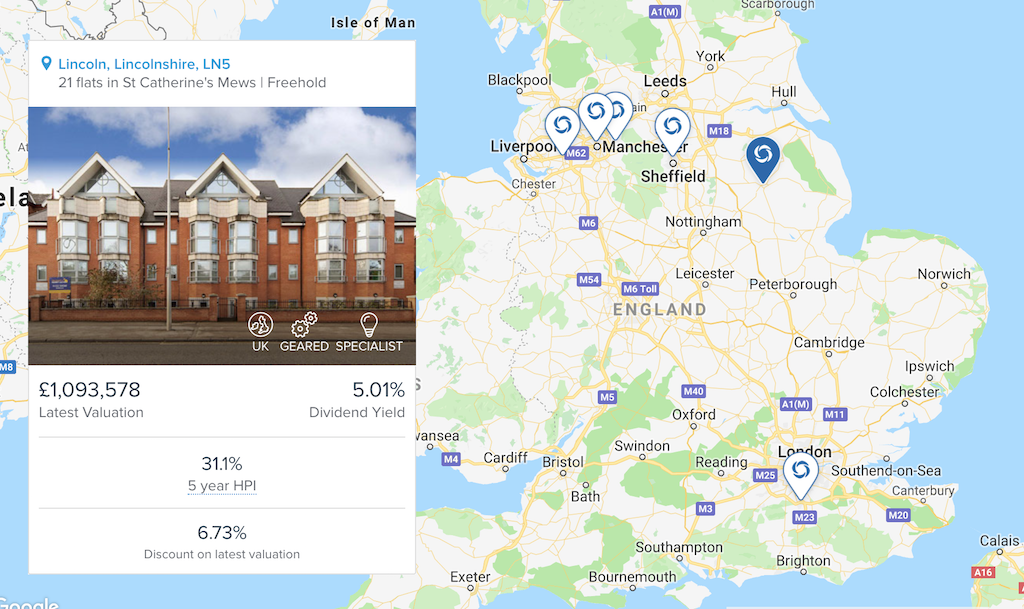

As you can see, I’ve split my investments between Manchester city centre, Greater Manchester, Sheffield, Warrington and Newcastle. I’m also bidding the rest £2,000 in Liverpool City Centre and Birmingham. And why not! London prices are dropping while midlands rise 6% in a year.

I believe with projects such as the HS2 and the regeneration that’s going on in the north, these are the areas that will greatly benefit. The government is making efforts to advance those cities.

Also, because of the fact that London has appreciated so much recently, these cities have lagged behind and have room to grow. This seems to be the opinion of property experts (hi Robs): Episode 240, Episode 164.

If I had to invest in property using a traditional mortgage, I’d probably need a lot more money to start with. I’d also lack the diversification of investing in 5 different cities.

I bought the Manchester property at an 8% discount to the latest valuation. In the Resale market. Oh yeah… I forgot to mention the most important thing. The Resale market!

Buying and selling property in the Resale market

One of the reasons I decided to go with Property Partner is because I have the option to buy and sell already funded deals. This amazing feature allows me to bid on properties lower than their estimated value and immediately benefit from a below-market-value deal if other investors want to sell their holdings.

Additionally, I don’t have to wait until a Primary market deal comes up. I can sign-up and start investing immediately. I can also sell my investments to other investors early without having to wait the full 5-year period.

However, when trying this feature I found that the bid-ask spread is sometimes high. So existing sellers want to sell high and potential buyers to buy low which makes for a stagnant market. However, you can sort properties by the bid-ask spread and by discount in the Data View and then go for the ones that are selling at lower values AND have liquidity. That’s what I did!

Here’s how the Resale market looks like. Pretty much like any trading exchange.

So you know what the latest RICS valuation is, and you can bid well below that. There are properties that trade at a premium, and others that trade at discounts.

An awesome feature I “discovered” is that your money is not tied up when bidding for properties. That way, I can bid £1,000 for all 10 properties I want to buy at lower prices, without having to have £10,000 in cash. All I need is £1,000.

There’s an additional 0.5% stamp duty tax for buying shares in the Resale market. I don’t really care much about that because the discount rate will compensate me for buying in the Resale market.

Risks

What if Property Partner goes bust?

This is one of my worries. Similar to other platforms, I found they have a contingency plan. Of course, I wouldn’t want to see that take place.

But in the worst case, an alternative property manager is scheduled to take over. SPVs will be unaffected and investors will continue to own the properties as before. That’s because each property is ring-fenced from the assets and liabilities of Property Partner. See further info here.

What if people don’t pay the rent?

You simply don’t get paid. It’s, however, comforting to know that 5 years in the market they have never underpaid on dividends. I guess there is a lower risk in those multi-unit buildings.

The risk of voids diminishes as the number of units increases. This makes sense, as percentage-wise even a single void would be catastrophic in a 3-unit development but not so much in a 50-unit one.

Brexit drives house prices down & interest rates go up

With the Brexit madness at its peak, I’m surprised housing has proven so resilient as an asset class. But there’s always the risk that Brexit will drive prices down. If interest rates go up then mortgages will get more expensive which will eat up our returns.

Risk of buying mortgaged properties

This goes without saying, but if you leverage using a mortgage your gains as well as your losses are amplified. It goes both ways. However, I’m happy to take the risk since I’m a long term investor and on average property goes up.

Final words

I must admit that I learned all these by reading the vast knowledge base and exchanging emails with the Property Partner team. They were quite responsive and I was impressed they were answering all my questions in detail before I invested a single penny.

To me, that’s a good sign of a platform that respects customers. Another good sign is the excellent rating on TrustPilot. They’re also authorised and regulated by the FCA.

I told them I’m considering investing serious money and they invited me to one of their events. So I went and met part of the 20-people team along with other investors. Property Partner also support ISA investments for their development loans part. Faraj from the team was very helpful and knowledgeable. I mentioned Foxy Monkey and he gave me his contact details to pass on to those interested

faraj.jabbour@propertypartner.co

So overall first impression is very positive. Time will tell.

Initially, my passive investor instinct was shouting at me. 0.7% to 1.2% annual fee? Are you serious?

But then I thought that’s a bargain considering I benefit from their expertise, getting below market value deals by buying in bulk and diversifying in multiple cities. In fact, I’m quite happy with the pricing model for investors that want to put in more than £10,000. Plus there is no minimum investment amount.

Read my review on the Property Partner fee structure

My strategy going forward will be to buy good deals in the primary market. I saw that good primary deals can sell for 10% or higher in the resale market just after being re-listed. Of course, one can get good deals in the resale market, so I’m exploring low bidding there as well.

My plan is to write an update every 3-6 months and occasionally monitor my Property Partner portfolio. There are deals that come up such as new development loans (10%+) they recently started. So stay tuned!

By the way, Property Partner is currently offering a 2% bonus if you invest £10,000 or more. So a nice little £200 extra for me to invest :)

Disclaimer: This is not investment advice. There is risk involved in investing. As always, do your own research. Property Partner did not pay me to write this experiment. If you, however, become a client through my links then I will receive a reward at no extra cost to you (and thanks!). You can also do the same; they operate a “Refer a friend” scheme.